You want to keep your family, your friends, and yourself safe in this crazy world of ours, so you obviously went ahead and got yourself a firearm, appropriate training, and a concealed carry (CCW) permit.

Now, you’re ready to step into the world knowing that you have the ability and right to defend yourself if the need arises – well, almost.

One of the most crucial aspects of being a concealed carrier is being prepared to defend yourself legally while defending yourself physically. This is where concealed carry insurance comes into play.

Below, we have an in-depth concealed carry insurance comparison among the best CCW insurance companies.

We are going to go over everything that’s involved with concealed carry firearm insurance: what it is, why you need it, and then go over some of the most prominent insurers on the market today for you to choose from.

By the time you finish this article, you’ll be even better equipped to protect yourself and those important to you!

CCW Safe

Plans starting at $16/month

(Price accurate at time of writing.)

What is Concealed Carry Insurance?

Before we get into the nitty-gritty comparison of concealed carry insurance companies, let’s start off by discussing what CCW insurance actually is and isn’t.

A relatively novel form of liability insurance, concealed carry insurance emerged and has rapidly grown alongside the rapidly increasing ranks of permitted concealed carriers across the United States. Naturally, these carriers needed some additional legal protection in the event they are forced to use their firearm in self-defense; thus, the need for new insurance to be created.

As you might have guessed, multiple companies either added this coverage to their policies or changed their insurance plans altogether, and some companies were started with CCW insurance in mind.

To put it simply, concealed carry insurance is very similar to other insurance policies, like your automobile, house, or life insurance that you already have. You pay a premium to financially and legally protect yourself in case an event occurs that causes damages.

Concealed Carry Insurance vs. Traditional Insurance

What separates concealed carry insurance from other forms of insurance is that it provides protection to the insured if they have to use their weapon for some sort of self or home-defense.

Depending on the policy you choose, you may be entitled to different forms of coverage from your concealed carry insurance provider. Some companies provide legal representation in both criminal and civil trials, however, this is not always the case. Depending on the insurance provider or level of coverage you choose, you may find yourself woefully undercovered.

Some policies will only reimburse you after the legal proceedings have been concluded, meaning that you’ll need to pay out of pocket. As you might guess, this could be expensive, and you may not have the funds to cover the legal proceedings yourself, so be careful when looking at policies that work this way.

Although most of the carriers we cover in our comparison below offer upfront payments, the insurance policy you were eyeing might not, so be sure to read very carefully or have an attorney check the policy with you.

In some cases, policies might only provide partial financial assistance and will instead give you access to a network of self-defense or firearms specialist lawyers with experience in these types of trials. It’s up to you to determine the level of protection you need from your policy and should select one accordingly.

Common aspects of most concealed carry insurance policies typically provide legal defense after you’ve used your concealed carry weapon. This is very common because, even if you used your weapon in self-defense, a criminal investigation is almost always conducted. Going through this process without gun insurance could be incredibly costly, confusing, and potentially dangerous for the self-defender–in a legal sense.

Some concealed carry insurance policies also cover your defense in the event that a civil trial follows the criminal case. Although you may be cleared of any charges at a criminal trial, a subsequent civil trial could find you liable for damages against the person(s) you were defending yourself against.

It’s hard to believe, but there have been instances where someone who legally defended themselves against an aggressor found themselves facing damages from a civil court decision that found them at fault. Due to this sad fact, it’s always a good idea to explore policies that include some coverage for these types of trials.

Why is Concealed Carry Insurance Important?

If you were wondering what could happen to you after you use your weapon for self-defense, let us paint a picture of a few things that might happen to you.

Like we mentioned before, in almost any instance a firearm is used, a police investigation occurs to gather evidence to be used in a trial. During this time, you may find the firearm you used confiscated as evidence, and you’ll likely have to give a statement about the events.

Once the trial begins, you’re likely going to have to miss school, work, or anything else you had planned. This is where the expenses that concealed carry insurance would cover comes into play, potentially including lawyer fees, court fees, bail bonds, and other associated legal fees.

Depending on how the trial goes, you may even find yourself convicted in the event that a jury finds you guilty of some part of your self-defense. Say, for example, you defend yourself with a firearm, or have some modifications/attachments, that are illegal in your area. Without representation, this might be an issue that could torpedo your entire defense and put you in jeopardy for being found guilty yourself.

Following this criminal trial may come the previously mentioned civil trial, whose treacherous legal waters could end up drowning you in legal fines and reparations. It’s important that you have representation in this situation because you could be found liable for other damages like pain and suffering to the aggressor or their family even though you defended yourself.

Concealed carry insurance policies that include coverage for these trials could very well save you from this unjust fate.

While insuring yourself for a concealed carry self-defense incident is important, you should also familiarize yourself with the different laws in your state as this can make a difference in the policy you need. With differing laws regarding not only concealed carry, but home defense and general firearm laws, you might find the policy you choose for yourself is at odds with other laws and regulations. It is always recommended you meet and discuss your situation with a lawyer before purchasing a policy.

How Much is Concealed Carry Insurance?

Costs for concealed carry insurance, as you might imagine, vary quite widely depending on what kind of coverage you want for yourself and possibly your family. As you’ve learned, though, what you pay monthly or yearly could be substantially less than what it may cost you if you are a concealed carrier who is forced to use their weapon for self-defense.

A monthly payment of less than $20 for insurance might seem like a waste, but when your facing trial, legal, attorney, and other fees that could reach into the 6-figures and could be present for months, it won’t seem like such a waste. Just like other forms of insurance, it may hurt to make those payments, but when a crisis does happen, you’ll be glad to have something covering your back.

To give you an idea of what you can expect to pay, our research has shown that you could easily get a concealed carry insurance policy that covers the general bases for around $20 monthly, on the low end, but you can upgrade to more expansive policies that are closer to $600 annually, which offer substantially more coverage.

Once again, there’s no “perfect” solution. It’s up to you to decide what you’re willing to pay for the coverage you deem acceptable. So that you can get a better understanding of what’s out there, continue reading as we list some of the leading concealed carry insurers on the market today and what some of their most popular policies cover.

Best Concealed Carry Insurance Companies

Now that we understand what concealed carry insurance is, what it’s used for, and how much it generally costs, we are going to run you through a brief summary of our top CCW insurance companies.

We’ll give you some general information about the company, a list of our perceived benefits and drawbacks, and will finish each off with details about the price of coverage as well as information about what you can expect for coverage during a trial.

Because we are dealing with insurance and all the magnitude of variables that come into play when comparing policies, we are going to give you an overview of the BASE level of insurance that you can purchase for yourself that provides full coverage.

We are taking this approach because many of these insurance providers offer tiered levels of coverage where you can pay more to get more coverage, while others only offer only one level or offer add-ons to that coverage.

If you want a more complete picture of the coverage options, please see the table we developed at the end of the article that offers more information on each firearm insurance provider.

-

4.2LEARN MORE

4.2LEARN MOREIf you knew anything about concealed carry insurance before getting this far into the article, U.S. Concealed Carry Association (USCCA) is probably the company you thought of when discussing this subject. I mean, the term “concealed carry” is right there in the name!

Well, you’re not wrong since USCCA is probably one of the biggest insurers in our list and has been doing it for a long time. Let’s dive a little deeper and explore their “Gold” membership option, which is also their lowest out of 3 tiers, to get a better idea of what you can expect.

Benefits

Although USCCA has some of the best coverage around, one of the drawbacks of this concealed carry insurance is that the upfront coverage only applies to the criminal defense costs and bail bond coverage, which actually comes directly out of that same criminal defense fund.

Another drawback is that the upfront payments only apply to the criminal defense coverage and your civil defense coverage is a reimbursement. You’ll eventually get covered for these amounts, however, it may require some patience on your part.

Lastly, as big as they are, we would expect them to send a team member to help customers with a major shooting incident, such as one of their competitors CCW Safe does. Unfortunately, they do not have a critical response team that comes to you, so you will need to do some of the leg work, for example, looking for a good lawyer in your city.

Drawbacks

Although USCCA has some of the best coverage around, one of the drawbacks of this concealed carry insurance is that the upfront coverage only applies to the criminal defense costs and bail bond coverage, which actually comes directly out of that same criminal defense fund.

Another drawback is that the upfront payments only apply to the criminal defense coverage and your civil defense coverage is a reimbursement. You’ll eventually get covered for these amounts, however, it may require some patience on your part.

Lastly, as big as they are, we would expect them to send a team member to help customers with a major shooting incident, such as one of their competitors CCW Safe does. Unfortunately, they do not have a critical response team that comes to you, so you will need to do some of the leg work, for example, looking for a good lawyer in your city.

Coverage Breakdown

- Monthly Cost – $10.95 (+ one-time start-up fee of $19.95)

- Criminal Defense Coverage Limit – Unlimited

- Civil Defense Coverage Limit – Unlimited

- Bail – Not covered (available in Bail Bond & Expert Witness coverage add-on)

- Lost Wages Compensation – Not Covered

-

4.0LEARN MORE

4.0LEARN MOREU.S. & Texas LawShield is an up-and-coming concealed carry insurance provider that you can feel safe with backing you up in court and beyond.

Started in 2009, U.S. & Texas LawShield was created by a group of like-minded lawyers tired of the way that “the system” treats law-abiding citizens who use a firearm as they were intended–for protection. They dedicated themselves to helping these citizens better fight the injustice they were facing, thus, U.S & Texas LawShield was born.

Benefits

One of the biggest draws of U.S. & Texas LawShield insurance is its incredibly attractive monthly price of only $10.95/month, however, they do tack on a one-time $19.95 start-up fee to activate the coverage.

This is the lowest monthly base price out of all the concealed carry insurance companies we reviewed, but they still manage to provide competitive coverage that includes Criminal and Civil defense fees upfront.

Drawbacks

That low monthly price does come at a cost, and that is that U.S. & Texas LawShield leaves out a lot of supplemental coverage that many of the competitors offer standard. Along with their basic coverage, you’re able to select add-on coverages such as Gunowner Identity Theft, Multi-State Protection, Bail Bond & Expert Witness, Minor Children, and HunterShield coverage.

For some, this ability to modify your coverage could be seen as a positive, but when we add the most common features found in other policies, which are Multi-State Protection and Bail Bond & Expert Witness coverage, you’re looking now at close to $18.50/month ($19.95 is distributed across 12 months) for coverage. So, when it comes down to it, the level of coverage you would need to match the competitors could end up being pretty similar to other concealed carry providers in our list.

Coverage Breakdown

- Monthly Cost – $14.95

- Criminal Defense Coverage Limit – $50,000

- Civil Defense Coverage Limit – $500,000

- Bail – $5,000

- Lost Wages Compensation – $250/day

-

3.5LEARN MORE

3.5LEARN MORELet’s say that someone breaks down your home’s front door and threatens your family. You take action and legally put down the intruder with your weapon to save your family. The first call you make is to the police to report the incident, but then who do you call after? SecondCall Defense wants to be that second call (get it?).

Positioned in what could be the “sweet-spot” between the big guys and the little guys, SecondCall defense prides themselves on doing the best of both worlds: the coverage you get from major insurers with the service you find with the smaller companies. As this company offers multiple tiers of coverage options, we are going to be reviewing their middle, “Full Coverage” option.

Benefits

Like other concealed carry insurance providers, SecondCall Defense’s full coverage policy offers to pay all fees upfront, which is a welcome relief when faced with the bill that comes due after court cases are completed.

This is a welcome benefit as their monthly price is right at or below the competition making this a competitive option. Another major benefit of SecondCall Defense is that it offers $50,000 in civil defense coverage in the event of a civil trial not going your way.

Drawbacks

As you may have guessed, the savings you gain from a lower monthly payment may end up coming around to hurt you when you need it most as the “Full Coverage” plan’s actual coverage is weaker than most of the big concealed carry insurers. Of course, you could always pay an additional $20/month to supercharge your coverage, but that is a different story.

Coverage Breakdown

- Monthly Cost – $14.95

- Criminal Defense Coverage Limit – $50,000

- Civil Defense Coverage Limit – $500,000

- Bail – $5,000

- Lost Wages Compensation – $250/day

-

5.0LEARN MORE

5.0LEARN MOREAnother great example of putting their money where their title is, CCW Safe is another well-regarded big boy in the concealed carry insurance realm. Calling themselves a “… legal defense service plan” instead of an insurance plan, CCW Safe is committed to helping defend concealed carriers after they’ve already defended themselves.

Although they offer great protection for LE and Military (both active and retired), we will review CCW Safe’s Ultimate plan since it can cover everyday concealed carriers.

Benefits

One big reason to pick up legal protection from CCW Safe is because they offer no limits on the amount spent on criminal or civil defense trials. This is pretty unique and makes their plans one of the best on the market.

And the biggest benefit to working with CCW Safe is their Critical Response Team. If you ever have to use your gun to defend your life, they won’t just help you with fees. They will send team members to you the next day to help guide you through the entire ‘second-fight’ process, step-by-step, which is huge.

Although you’re practically covered completely, don’t let it be the reason to have an itchy trigger finger in moments of stress or crisis. CCW Safe simply wants to offer their clients the best protection possible because they believe Americans forced to protect themselves deserve to be protected at all costs, something we understand entirely.

Drawbacks

Other than being one of the pricier plans out there, the major drawback to CCW Safe’s Ultimate defender plan is that you MUST be a permitted CCW carrier in order to be covered. Of course, this doesn’t really apply to this comparison as the article is written for legal concealed carriers, but we thought we should mention it nonetheless.

Coverage Breakdown

- Monthly Cost – Plans starting at $16/month

- Criminal Defense Coverage Limit – No Limit

- Civil Defense Coverage Limit – No Limit

- Bail – $500,000

- Lost Wages Compensation – $300/day (up to $1,500)

-

3.5LEARN MORE

3.5LEARN MOREThe name says it all regarding Firearms Legal Protection and concealed carry insurance. They offer firearms legal protection and do it pretty well for the price that they charge.

They aren’t one of the biggest insurers out there, but they offer good coverage and benefits all at a reasonable monthly price that is quite attractive to most. We will be covering Firearms Legal Protection’s “Individual Basic” plan, but they offer other tiers that offer more at a higher price.

Benefits

One of the major benefits of Firearms Legal Protections’ “Individual Basic” plan is that it’s on par with SecondCall Defense’s close-to-industry low of $14.95/month while offering uncapped attorney fees for both criminal trials and civil suits.

It also allows a covered person to use any legal weapon in their arsenal to defend themselves, so you don’t need to worry about being left out if you protect your family with something other than your firearm.

Drawbacks

Although the “Individual Basic” plan offers a lot at the low monthly price, glaringly absent is the bail bond coverage that other plans usually include to some degree in their plans. Another drawback is that for the coverage to extend to other states, in addition to a covered person’s state, one must upgrade to the next insurance tier.

Coverage Breakdown

- Monthly Cost – $14.95

- Criminal Defense Coverage Limit – No Limit

- Civil Defense Coverage Limit – No Limit

- Bail – Only available in upper tiers (up to $250,000)

- Lost Wages Compensation – $350/day (subject to Occurrence Limit)

-

3.5LEARN MORE

3.5LEARN MORERight off the bat, we need to state that Armed Citizens’ Legal Defense Network (ACLDN) is NOT a traditional concealed carry insurance provider. Rather, it classifies itself as “the funding mechanism for the legal defense…”, which we’ll get into more below, but we wanted to get that out of the way first. Although not a “traditional” form of concealed carry insurance, ACLDN does have some factors that might be appealing.

Benefits

Comprising some big guns from the legal community specializing in legal, self-defense and firearms arenas, ACLDN’s vast network of experts will be at your disposal if you are a member facing a self-defense trial after using your firearm. This means that even if they do not provide the strongest or even most comprehensive coverage, you can rest easy knowing you have the best defending you.

Another benefit, depending on how you look at it, is that this is by far the cheapest option out there for concealed carry support. There’s a school of thought that the money you’d save with this option could be better used for investments or more guns.

Drawbacks

As we mentioned earlier, ACLDN is NOT a true concealed carry insurance policy even though it offers some coverage and support. You will not be covered for any civil damages you might incur during a civil trial and are only given $25,000 (more pending approval) for your criminal and civil trials, each. You’re also not going to find other coverage benefits that actual concealed carry insurance providers offer like lost compensation support or firearm replacement services.

Coverage Breakdown

- ANNUAL Cost – $135.00 ($11.25/month)

- Criminal Defense Coverage Limit – $25,000 immediately, more pending approval

- Civil Defense Coverage Limit – $25,000 immediately, more pending approval

- Bail – Not Covered

- Lost Wages Compensation – Not Covered

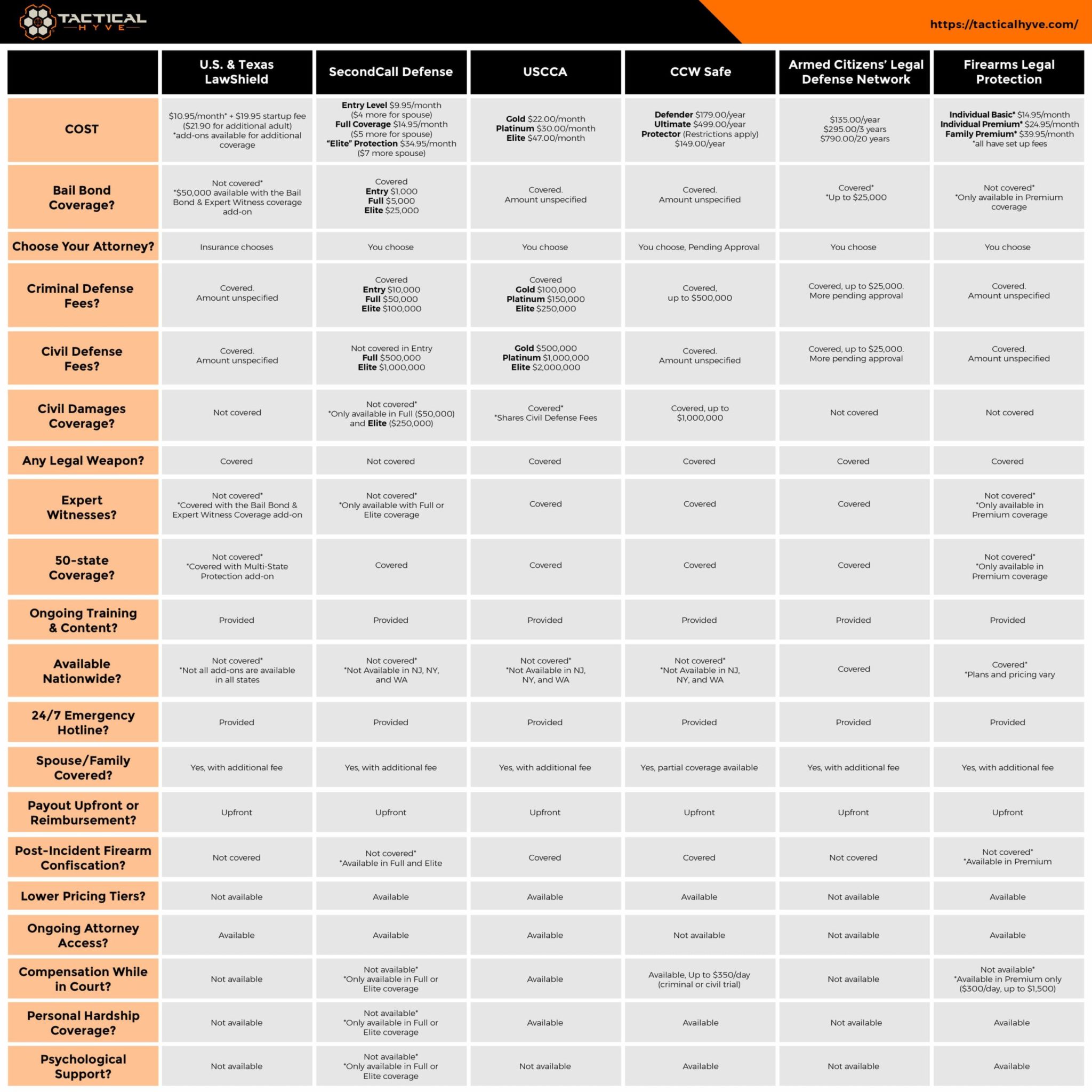

Comparison Chart

As you may have noticed when reading through our brief summaries of each major concealed carry insurance company, overlap is expected and they all might seem largely the same. The truth is: yes, on the surface, most of these insurance plans are very similar. However, this is not to say that they are all exactly the same.

To help you better determine which concealed carry insurance is the best (and right for you) we’ve developed a chart that shows more information about each insurance company. Take a look below. (Click the table to view the full-size image.)

Share this Image On Your Site

CCW Safe

Plans starting at $16/month

(Price accurate at time of writing.)

Conclusion

Wrapping this all up, CCW Safe is our preferred concealed carry insurance carrier because of their comprehensive coverage, a sole focus on protecting their members during the ‘second fight’, and the fact that they have a Critical Incident Team standing by to be with you if you’re involved in a shooting.

They won’t just write you a check and leave you to do the bulk of the work.

But, even though we think CCW Safe offers the best legal protection, one of the others we covered (or maybe one we missed) may be better suited to you and your family’s needs.

These insurance policies are always in flux, so what’s included in our article today might change a few months later. We’ll do our best to keep it updated but remember, it’s up to you (and possibly your attorney) to read and analyze your potential CCW insurance policy to have the coverage and benefits you need.

We recognize that other concealed carry insurers might have provisions and policies that set them apart from those on our list.

We’re always interested in learning more, so please share them and any other thoughts you may have about this topic in the comments below!

I’m interested in this insurance. I have Utah CCW and I live in California. How this will work for me?

Hello Gregg,

I can help you find the answers you are looking for. Please feel free to contact me @ [email protected].

Are any of these plans available for NY CC permit holders. I know USCCA is out of the question they not available in NY

I have CCW Safe and I only pay $14 per month for unlimited coverage. Every review I’ve seen uses the most expensive plan you can get as a reference which misrepresents their coverage since their lowest plan has equal or better coverage.

I reside in New York State, but I’m not looking for a policy for coverage in New York State,

The firearms will not be stored, carried, used in New York State.

The policy is for when I’m in Tennessee and other states that my Utah non-resident permit is allowed.

The firearms will be stored, locked in Tennessee.

Is there a company that will sell me insurance ?

We are unsure. Best bet is to contact each provider and talk to them about your situation.

I am an elderly person with a NY target permit. Are there any age restrictions in any of the insurance policies.. Also do the policies cover rifles and shotguns.

I was with USCCA until the underhanded stunt they pulled in Nov. 2021, when they inserted a reimbursement clause into their policy and neglected to inform anyone about the change. Bottom line, if you’re found guilty or if you take a plea deal when faced with a corrupt prosecutor with an agenda backed by the anti-gun media, you have to reimburse the USCCA for all coverage supplied. Worst of all, they sold out EVERY state where they had coverage, in order to remain active in Washington, which along with (I believe) NY and NJ, have laws prohibiting insurance for those found guilty of a crime. Instead of dropping Washington from coverage like CCWSafe did, USCCA changed their policy in every state they’re in, so now the reimbursement clause is in every USCCA policy in every state. I switched to CCWSafe immediately, after speaking to one of the attorneys there.